The Algorithms

INTRODUCTION

This page outlines the structure of the project and its software. It describes the architecture as well as the basic functionality of the modules. However, the exact workings of the signals are not discussed here. Additionally, the repository is not publicly accessible.

This page is still under construction. More information will be added gradually 🔍👀

TESTING AND OPTIMIZATION - FORGET MONOPOLY MONEY

I’ve moved past demo trading. With monopoly money, anyone can be profitable. Demo account trading often does not provide meaningful results, while directly trading futures contracts with personal capital is currently too risky and capital-intensive for me. But how can I test my signals and algorithms and further develop my trading style without financially ruining myself? I mean, I need to forward-test the algorithms in addition to all the research and backtesting.

Therefore, I trade the systems live in the market daily at the US Open using proprietary-funded accounts to increase emotional pressure. I use the ATAS trading platform, which allows the integration of my algorithms and provides a convenient interface to access the market data (more on that in the algorithm part of my website). Prop trading has proven to be an extremely helpful solution in this context. This model provides access to trading capital but requires successfully completing the qualification phase under strictly limited risk parameters. Proprietary-funded accounts must be built sustainably and managed with rigorous risk management to be retained in the long term. This presents a significant challenge that demands both discipline and consistent action. I'm aiming to fund a prop trading account to ensure the algorithms perform consistently over time, across various market conditions, and even under the influence of human error. In a lot of cases, the system works, but the trade execution suffers due to inaccuracies caused by my own incompetence 🙄

TRADING SIGNALS

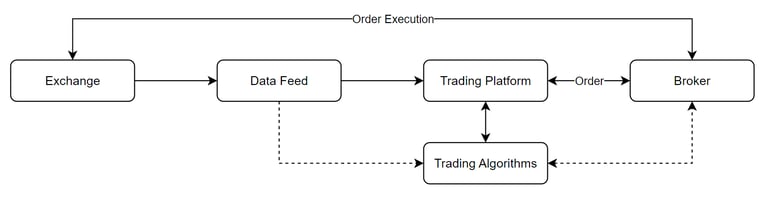

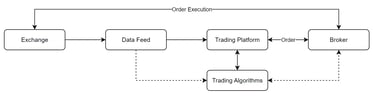

Since this is not a typical software project, only the structure and project architecture are described here. A key feature of the project is its modular design, which ensures flexibility and expandability. The chart below illustrates how an algorithm implementation integrates into the overall process. The data feed provides current market data (such as prices, volume, etc.), which is sourced from the exchange and visualized in the trading platform. I use the Rithmic data feed and ATAS as charting software.

The trading platform acts as an interface between the trader and the broker. This connection is bidirectional: the trader sends orders to the broker, while the broker returns execution details and confirmations. The broker receives the orders and forwards them to the exchange for execution.

Currently, the algorithms run through the trading platform’s interface. Once the algorithms have reached sufficient maturity, they will be directly connected to the data feed to reduce overhead. This will allow the data to be processed more quickly in the future, enabling orders to be transmitted to the broker with higher performance. That is shown in dashed lines in the image.

THE TRADING SYSTEMS

Currently, there are two systems: one analyzes the market environment, while the other generates concrete trading signals.

In trading, context and market structure are two key factors that can determine success or failure. Context refers to the broader market environment, whereas market structure reveals how supply and demand behave in real time. Market structure reflects the actual behavior of market participants across different timeframes. It includes critical technical elements such as support and resistance levels, liquidity, and trader behavior at various price zones. Together, context and market structure form the foundation of informed trading decisions. Without proper context, a trader may easily trade against the main trend. Ignoring market structure can lead to poor entries and increased risk. Solid analysis allows for precise entries and exits.

To simplify this analysis, a system has been developed that enables fully automated market evaluation. This helps me make well-informed decisions every day.